What went wrong with Fed policy in 2021-2

Looks good! The Fed brought nominal indicators back to trend (maybe a notch above, but could that really matter all that much? after all, didn’t the pandemic result in a bit of a productivity boom?) and is now stabilizing them! Way to go for the Fed! Post-2008 errors: averted.

…doesn’t look so good, now, does it? Who could have remembered that between 2010 and 2020, the U.S. was at above-trend growth, which could not have possibly been sustained over the next few years, even without the pandemic? When real fundamentals deteriorate, it makes no sense to go back to the previous nominal trend -a good lesson for Chinese monetary policy, and a reminder Japanese monetary policy wasn’t as bad as often made out to be. And that pandemic-era productivity boom? Ephemeral, and to a great extent simply a composition effect.

…Scheiße. Now we see what a real “great vacation” looks like.

Those forecasters who upgraded the U.S.’s growth performance in response to the pandemic should be fired. If they haven’t already been.

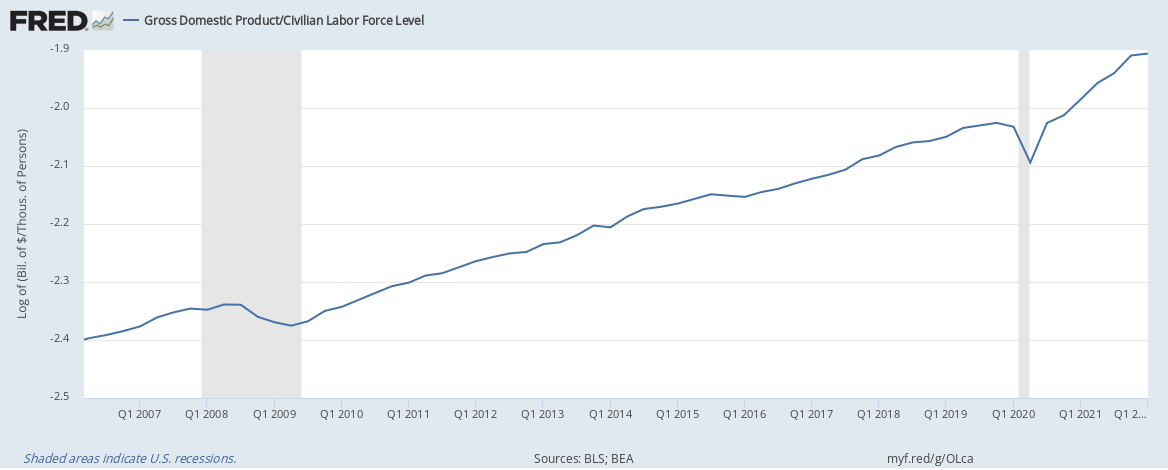

This case study really shows the central flaw in simplistic NGDP level targeting: the target has to be dynamically responsive to the requirements of the labor market. If the U.S. was flooded by 200 million Chinese, it would make no sense to keep the target the same. The better measure is nominal GDP per labor force participant. Which looks like this: